Ruling Date

May 30, 2024

Product Name

Cocoa Preparations

HS Code

1806.10-

Origin Rule for Final Product

(TPP11) A change to sweetened cocoa powder of subheading 1806.10 containing 90 per cent or more by dry weight of sugar from any other heading, except from heading 17.01;

Materials List

| Material Name | HS Code | Description | Origin Certification |

|---|---|---|---|

| Sugar | 1701 | Sugary substances (contains sugar) | FTA Contracting Country |

| Cocoa Powder | 1805 | Cocoa substances (non-sweetened) | Non-Contracting Country |

Manufacturing Process

| Description |

|---|

| Sieving sugar and cocoa powder |

| Mixing |

| Forming cocoa preparations |

Recognition Reasons

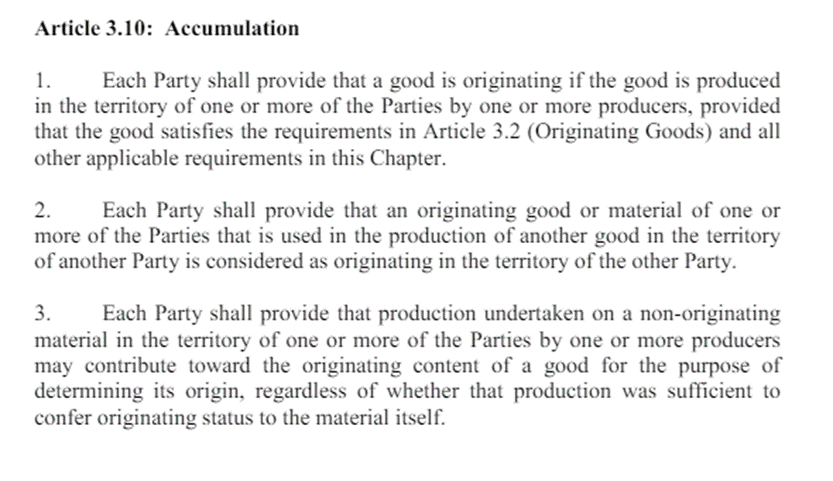

The HS code for the cocoa preparation is 1806.10-, thus the product-specific origin rule is “A change to sweetened cocoa powder of subheading 1806.10 containing 90 per cent or more by dry weight of sugar from any other heading, except from heading 17.01;”. Upon examining this product, it is found that sugar (heading 17.01) is used. According to the product-specific origin rule, the use of non-originating materials from heading 1701 to manufacture cocoa preparations (HS: 1806.10) does not satisfy the requirements to be recognized as an originating product under TPP11.

In other words, sourcing sugar (heading 17.01) from non-TPP11 member countries and manufacturing cocoa preparations in Vietnam would not satisfy the origin rules. Therefore, in this case, sugar (heading 17.01) is sourced from TPP11 member countries to be recognized as originating materials under the TPP11 agreement. By applying the Accumulation provision, the TPP11 agreement, which includes many countries, allows for the selection of countries where materials can be procured cost-effectively to meet origin rules.

By applying the accumulation provision, the sugar is recognized as originating under the TPP. Furthermore, the non-originating materials (cocoa powder) from Non-Contracting Countries meet the product-specific origin rule criterion (CTH), thus the cocoa preparations are recognized as originating products under the FTA.

Conclusion

This cocoa preparation combines materials sourced from TPP11’s FTA Contracting Country and Non-Contracting Countries, fulfilling specific origin rules, and thus is eligible for preferential tariff rates under the FTA.

If this FTA were a bilateral agreement, the procurement options for sugar (heading 17.01) would have been limited. However, as this is a multi-country FTA, it allows for significant tariff reduction.

Moreover, it’s crucial to pay attention to the product-specific origin rule’s “from any other heading, except from heading 17.01” clause, rather than just recognizing CTH, to ensure the product is recognized as an originating product.

By following this manufacturing process, the trading company was able to significantly reduce manufacturing costs compared to conventional import methods, and by applying preferential tariff rates, they achieved further tariff reductions. This enabled the trading company to realize cost savings and enhance competitiveness.

Leave a Reply