A trading company in Importing Country A is attempting to import neckties from Italy, an FTA Contracting Country. These neckties are manufactured in Italy. In the production process of the neckties, materials sourced from non-FTA countries including:

- WOVEN FABRIC/MAIN

- INTERLINING

- BRAND LABEL

- CARE LABEL

- SEAMTHREAD

Are used. Will these neckties qualify for tariff reduction under the FTA’s rules of origin when imported in this manner?

2. Ruling Issuance Date

May 21, 2024

3. Product Name

Necktie

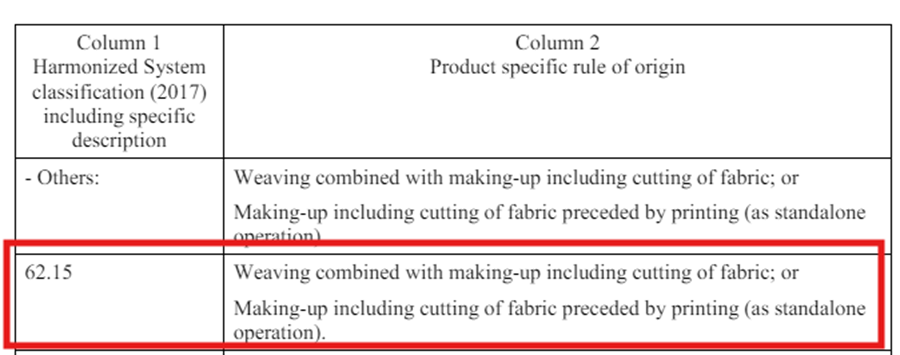

4. HS Code

6215.10

5. Product-specific Rule of Origin

“Weaving combined with making-up including cutting of fabric; or…”

Note: This rule is found in one of the agreements concluded by the EU among various FTAs. The rules may vary depending on each FTA. The product-specific rules do not use the change in tariff classification (CTC) or value-added (VA) criteria but specify only certain manufacturing processes.

6. List of Raw Materials

| No | Material Name | HS Code | Description | Origin Determination |

|---|---|---|---|---|

| ① | WOVEN FABRIC/MAIN | Ch.50 | Woven fabric | Non-Contracting Country |

| ② | INTERLINING | Ch.55 | Interlining | Non-Contracting Country |

| ③ | BRAND LABEL | Ch.58 | Polyester brand label | Non-Contracting Country |

| ④ | CARE LABEL | Ch.58 | Polyester care label | Non-Contracting Country |

| ⑤ | SEAMTHREAD | Ch.54 | Seam thread | Non-Contracting Country |

7. Manufacturing Process

① WOVEN FABRIC/MAIN

- Cutting

- Weaving

- Finishing the fabric

- Sewing into the shape of a tie

- Final finishing and inspection

② INTERLINING

- Cutting

- Weaving

- Finishing the fabric

- Sewing into the shape of a tie

- Final finishing and inspection

The following three items have not undergone significant processing changes in Italy:

- ③ BRAND LABEL

- ④ CARE LABEL

- ⑤ SEAMTHREAD

8. Certification Reason

The necktie’s HS code is 6215.10, therefore the product-specific rule of origin is “Weaving combined with making-up including cutting of fabric.” An interesting aspect of the product-specific rules of origin applied in this agreement is that they do not use the change in tariff classification (CTC) or value-added (VA) criteria. Instead, they specify only certain manufacturing processes. This makes it challenging to meet the origin criteria when using non-originating materials that do not undergo significant processing in Italy, an FTA signatory country.

Upon reviewing the details of the raw materials, it is clear that the non-originating materials meet the criteria set by the product-specific rule of origin, thus the necktie qualifies as an FTA originating product. Specifically, ① WOVEN FABRIC/MAIN and ② INTERLINING are produced in non-contracting countries and undergo weaving and cutting processes in Italy, meeting these requirements.

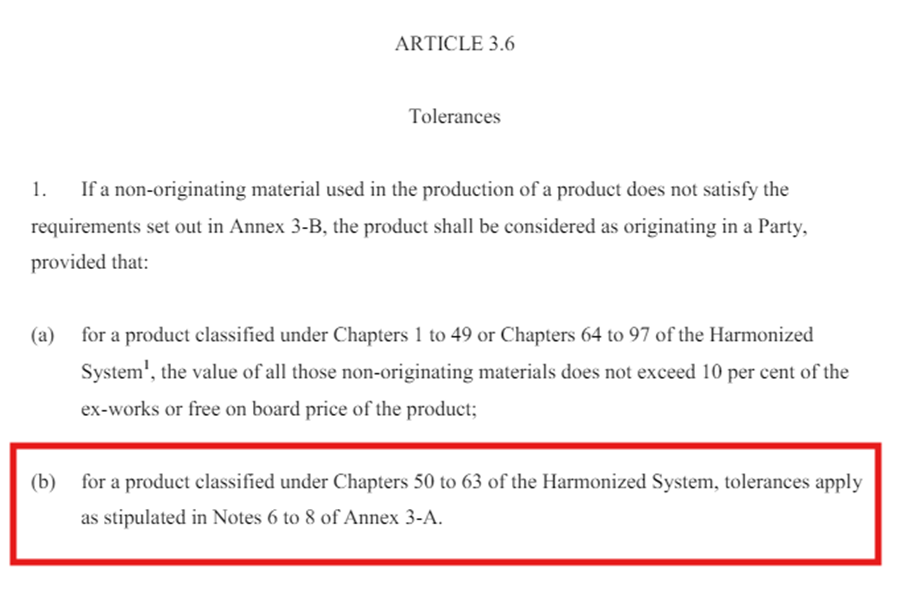

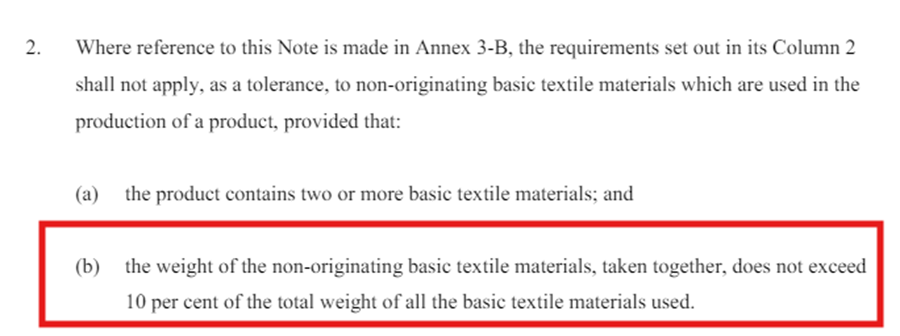

③ BRAND LABEL and ④ CARE LABEL, being less than 10% of the total weight, comply with Article 3.6 Tolerances (often referred to as de minimis in non-EU agreements) and ANNEX 3-A Note 7-2 regulations.

ANNEX 3-A Note 7 (2)

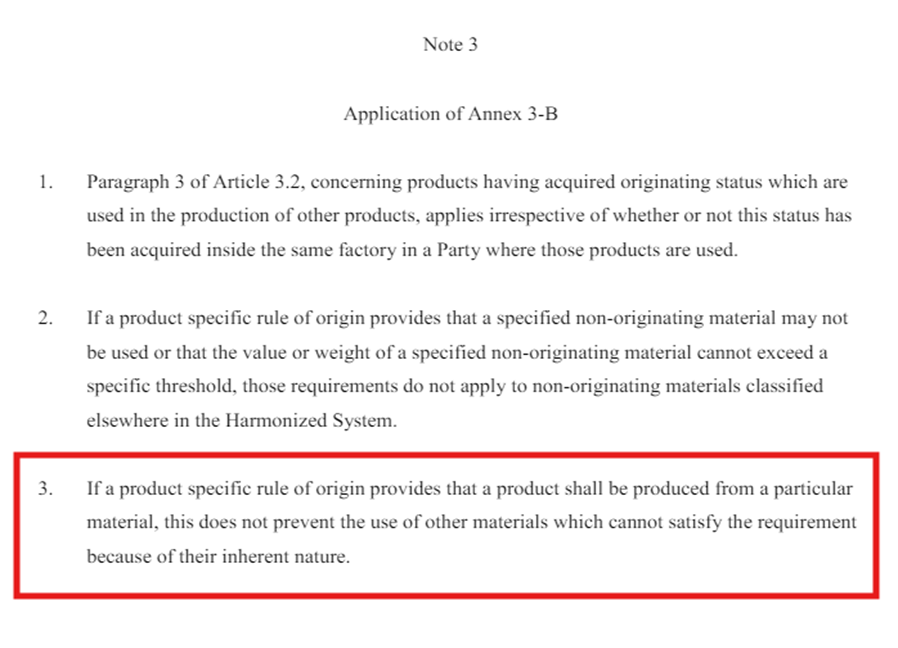

⑤ SEAMTHREAD (Sewing Thread) was determined to meet the rules of origin despite being a non-originating material. The reason for this is that ANNEX 3-A Note 3-3 states “If a product specific rule of origin provides that a product shall be produced from a particular material, this does not prevent the use of other materials which cannot satisfy the requirement because of their inherent nature.” It was determined that SEAMTHREAD falls under this exception.

9. Conclusion

This case is intriguing because ③ BRAND LABEL and ④ CARE LABEL, being less than 10% of the total weight, are passed through applying tolerances (de minimis) to meet the rules of origin, and ⑤ SEAMTHREAD, despite not meeting the rules of origin, qualifies under ANNEX 3-A Note 3-3 which states that “The use of certain materials is not prevented if due to their inherent nature they cannot meet other rules.” This is due to their critical role in the product’s manufacturing process and the impossibility of their substitution.

Additionally, in cases like the current example where the product-specific rules do not use the change in tariff classification (CTC) or value-added (VA) criteria but specify only certain manufacturing processes, the provision allowing non-originating materials to be deemed as originating if they “cannot meet other rules due to their inherent nature” is a fascinating relief measure with potential broad applications. However, determining whether such conditions are met is crucial and requires thorough consultation with customs authorities. Applying this relief measure necessitates meticulous discussions with customs to ensure compliance. FTAs’ rules of origin contain various types of relief measures, so even if it appears that the rules of origin are not met at first glance, there may be hidden provisions that provide relief. It is important not to overlook these possibilities.